Ensuring that retirement savings can sustain a lengthy retirement remains the paramount concern for current retirees and those nearing retirement. This objective has become more complex due to recent years of inflation, which has diminished the value of cash reserves. Currently, costs remain high in critical spending categories that most affect retirees, such as healthcare, housing, and basic necessities.

Although equities and fixed income securities are well-suited to address this challenge, certain retirees may be conservative in their risk tolerance, while others may question whether their portfolios and savings can adequately counter rising living expenses. For those with long-term investment horizons, comprehending how inflation impacts retirement income and how to structure portfolios to preserve purchasing power continues to be critically important. What key considerations should current and future retirees understand about managing today's financial landscape?

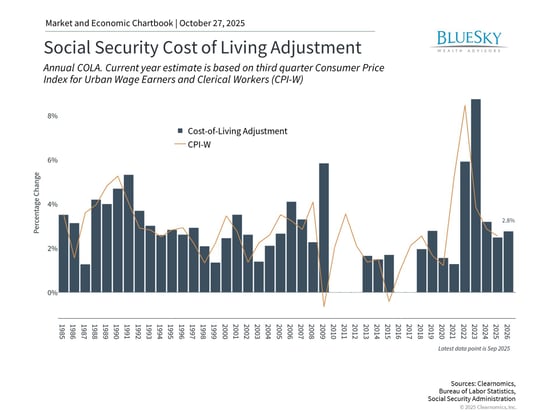

Experienced inflation may exceed Social Security cost-of-living adjustments

Recently, the Social Security Administration announced a 2.8% cost-of-living adjustment (COLA) for 2026, indicating ongoing inflation pressures. Although any increase provides some benefit, the inflation measured by economists frequently diverges from what individuals experience in their daily lives. In particular, this adjustment will increase the average monthly benefit to $2,064, representing just a $56 rise. This is modest compared to the 8.7% adjustment in 2023, which marked the largest increase since 1981.

The difficulty for retirees lies in the fact that although the pace of price increases may decelerate, prices themselves seldom decline. The COLA calculation uses a Consumer Price Index variant called the CPI-W, which monitors prices for working-class households. Nevertheless, this metric fails to recognize that retirees frequently encounter different inflation rates compared to younger workers. Healthcare expenses, housing costs, and other categories that constitute significant portions of retiree spending have frequently increased more rapidly than the overall index indicates.

For instance, medical care services increased 3.9% over the past year, health insurance rose 4.2%, and home insurance jumped 7.5%. Food prices climbed 3.1% during this timeframe, but meat, poultry and fish increased 6.0%. The expense of full service restaurants also grew 4.2% higher.

Compounding this issue, Medicare Part B premiums may increase $21.50 per month in 2026, rising from $185 to $206.50 based on recent Medicare trustees' projections. Because this amount is usually deducted directly from Social Security payments, this would consume roughly 38% of the average $56 COLA increase, ultimately leaving retirees with diminished purchasing power.

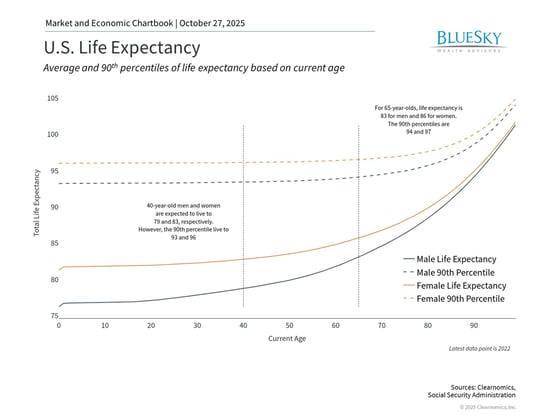

Extended life expectancies heighten the need for portfolio appreciation

Similar to how returns can compound over extended periods, losses also compound when a portfolio's purchasing power fails to match inflation. This consideration carries additional weight today because retirees must prepare for potentially longer lifespans than earlier generations. Therefore, life expectancy represents a crucial factor in any financial strategy.

Based on current Social Security Administration statistics, 40-year-old men and women have average life expectancies of 79 and 83, respectively. Yet, for individuals reaching 65 years of age, their life expectancies extend to 83 and 86. These figures represent averages - individuals in the 90th percentile may live to 94 and 97, respectively.

Although the prospect of experiencing a longer, healthier retirement represents a remarkable achievement over the past century, the distinction between a 20-year retirement and a 30-year or extended retirement carries significant implications for portfolio design and withdrawal approaches. This concept is frequently referred to as "longevity risk," a challenge that is asymmetric because depleting funds during retirement creates far greater problems than bequeathing assets to family members or charitable organizations.

Therefore, although many emphasize income-producing investments such as fixed income securities for retirement planning, maintaining growth-focused assets like equities remains equally important. This also introduces financial complications that make careful planning increasingly valuable. Knowing how to design portfolios for multi-decade retirement horizons, while controlling withdrawal rates and adjusting to evolving market circumstances demands knowledge that extends well beyond basic guidelines.

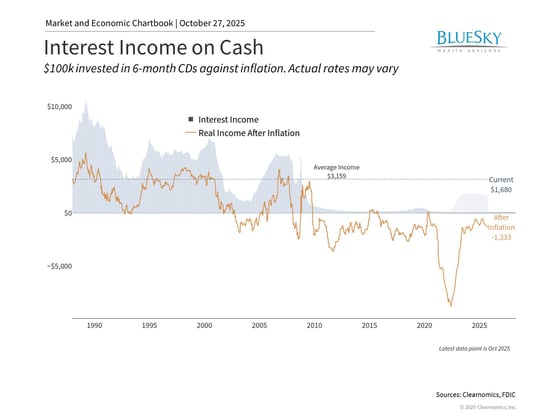

Declining short-term rates will diminish cash account income

Recent Consumer Price Index information, which experienced delays due to the government shutdown, carries implications for Federal Reserve policy and broader interest rates. With inflation subsiding and employment conditions softening, the Fed is anticipated to continue progressively reducing policy rates. This transition, although beneficial for numerous economic sectors, will probably decrease the interest income generated from cash and money market accounts going forward.

For retirees who have relied upon interest earnings from their cash positions in recent years, this movement toward a lower interest rate climate may create difficulties. Although maintaining cash reserves for immediate expenses and emergencies continues to be important, depending excessively on cash results in forgoing the appreciation potential of equities and the compelling yields currently available across many fixed income sectors.

The pairing of moderating yet ongoing inflation with falling interest rates establishes a difficult landscape for conservative investors. Cash erodes in purchasing power due to inflation, and the interest it produces will decrease as the Fed proceeds with rate reductions. This elevates the importance for retirees to maintain a balanced portfolio incorporating growth-focused assets like equities, which have historically exceeded inflation over extended timeframes, together with fixed income securities that can deliver income and stability.

The bottom line? Although Social Security COLA offers some protection against inflation, retirees find it challenging to depend on this measure alone. Given increasing life expectancies and falling short-term interest rates, investors require portfolios capable of delivering both income and appreciation.

BlueSky Disclosures

Copyright (c) 2025 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company's stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security--including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

Recent Blog Posts: