For those in or approaching retirement age, there is nothing more important than building a portfolio that can support a long, fulfilling retirement. Given the difficult inflationary conditions of the past few years, the risk that worries most retirees continues to be outliving their savings. Until recently, the market and economic environment presented classic challenges to retirement planning, including high inflation rates and volatile financial markets. While stocks have rebounded to new all-time highs, and bond yields remain above historical averages, retirees may still be concerned about whether their portfolios will keep pace.

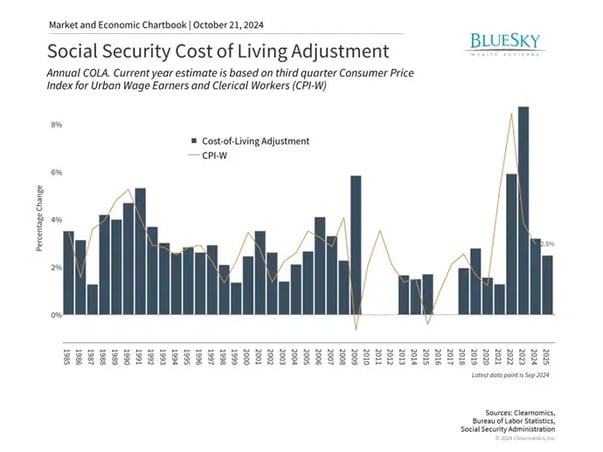

The 2.5% Social Security adjustment reflects slowing inflation

Many of these concerns stem from uncertainties such as the presidential election, Fed rate cuts, market valuations, and more. While we can’t control these events, we can control our own behavior. History shows that constructing and following a sound financial plan that can adjust to changing conditions, along with proper financial guidance, is still the best way to minimize retirement risks. How can retirees continue to maintain peace of mind and their quality of life in today’s challenging environment?

There is no bigger problem for retirement planning than inflation. Rising prices erode the purchasing power of savings and make it more difficult to plan for the future. To account for the higher cost of goods and services, the government makes an annual adjustment. The Social Security Administration recently announced a 2.5% Cost-of-Living Adjustment (COLA) for 2025. This increase will benefit more than 72.5 million Americans who receive both Social Security and Supplemental Security benefits from the government.

While all adjustments are helpful, this 2.5% increase is lower than those of the past three years, including an 8.7% adjustment in 2022, the largest since 1981. These were in response to rapid price increases in the aftermath of the pandemic amid supply chain disruptions, significant government stimulus, and Fed monetary actions.

The cost of living adjustment attempts to measure the effects of inflation on working-class Americans, based on the CPI-W index for households with “clerical or wage occupations”. The lower adjustment for 2025 reflects the fact that inflation has decelerated significantly since 2022. However, it’s impossible for a one-size-fits-all policy to work for everyone, since every household has differing needs. This is especially true given the increasing cost of housing and healthcare.

Thus, it’s more important than ever for investors to maintain a portfolio that can support their needs through retirement, especially as life expectancies increase. For those who still have years or decades until retirement, this highlights the importance of saving and investing early to maintain purchasing power over long periods.

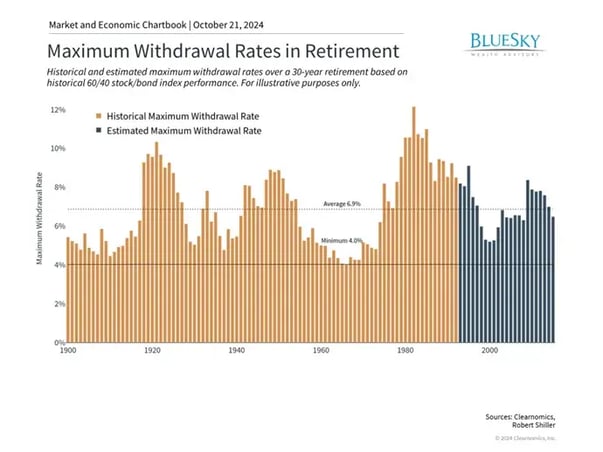

Withdrawal rates depend on market conditions

Another aspect of maintaining purchasing power and quality of life is determining how much can be withdrawn from a portfolio in retirement. Perhaps the best-known rule of thumb is “the 4% rule.” This concept was coined by William Bengen who observed that, historically, a 4% annual withdrawal rate from a portfolio was “safe” in that retirees were unlikely to exhaust their savings over a 30-year retirement horizon, accounting for inflation. For this reason, this is also sometimes referred to as the “SAFEMAX rate.”

The accompanying chart shows the historical “safe” withdrawal rates based on 60/40 stock/bond portfolios and inflation rates across 30-year periods, as well as estimates for more recent years. These illustrative figures show that only once in the 1960s did the maximum withdrawal rate fall as low as 4%. Of course, the safe withdrawal rate can vary dramatically from year to year, a fact that should not be surprising given how much market returns can change across a cycle.

This depends heavily on sticking to an investment plan throughout the full period. Investors who would have overreacted to short-term market pullbacks would have failed to rebound alongside the market, negatively impacting their withdrawal rates later in retirement. This analysis is also oversimplified since it does not account for differences in portfolio construction and risk tolerance across individuals that are a critical part of real-life financial planning. For instance, a 60/40 portfolio may be quite aggressive for many retirees, especially later in life.

However, what it does show is that despite the many market and economic challenges of the past several years, “safe” withdrawal rates are still quite strong. Not only did the stock market recover quickly after 2020 and 2022, but bonds have performed better more recently as well. Maintaining an appropriate asset allocation that can provide both growth and income is still critical for all savers, including retirees.

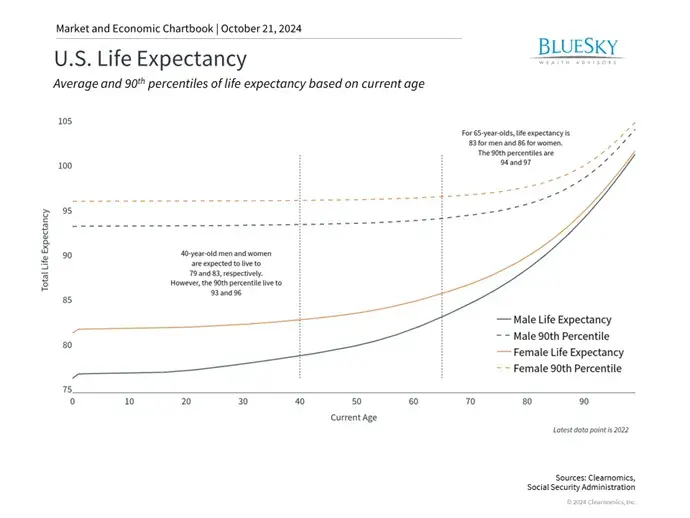

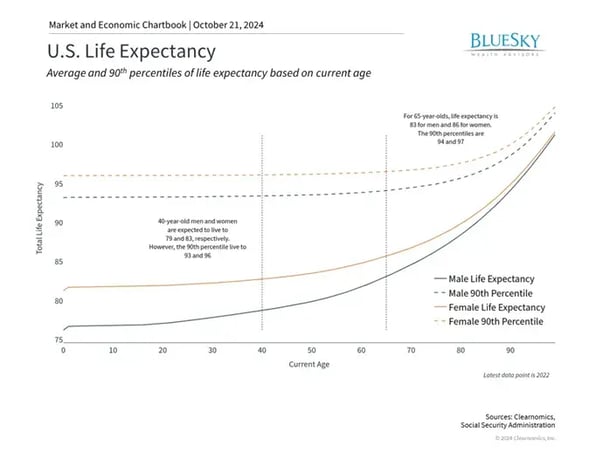

Longevity risk has increased as life expectancies grow

What simple rules of thumb like the 4% rule also don’t account for are increasing life expectancies. According to the Social Security Administration, 40-year-old men and women today have a life expectancy of 79 and 83, respectively, as shown in the accompanying chart. However, the 90th percentile could live well into their 90s. Similarly, men and women who are 65 years old today could live to 83 and 86, on average, while the 90th percentile could live to 94 and 97, respectively.

The difference of a decade or longer, e.g., a retirement of 20 years vs. 30 years, can have dramatic implications for investment portfolios and financial plans. While the prevalence of longer, healthier lives is a fantastic development, it can present challenges from a financial perspective and is referred to as “longevity risk.” This risk is asymmetric in that running out of funds is far worse for most households than leaving money behind to loved ones, charities, and more.

This means that life expectancy is an important input to any financial plan. Ultimately, managing longevity risk is another reason why all individuals can benefit from professional financial advice. So, not only do retirees need portfolios that can generate income, but they continue to need growth to ensure that their assets can maintain their quality of life over decades.

The bottom line? Inflation is slowing but costs remain high. Retirees and those planning for retirement will need portfolios that can generate both income and growth. As life expectancies increase, having a portfolio that can support a long and fulfilling retirement becomes even more important.

Copyright (c) 2024 Clearnomics, Inc. All rights reserved. The information contained herein has been obtained from sources believed to be reliable, but is not necessarily complete and its accuracy cannot be guaranteed. No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness, or correctness of the information and opinions contained herein. The views and the other information provided are subject to change without notice. All reports posted on or via www.clearnomics.com or any affiliated websites, applications, or services are issued without regard to the specific investment objectives, financial situation, or particular needs of any specific recipient and are not to be construed as a solicitation or an offer to buy or sell any securities or related financial instruments. Past performance is not necessarily a guide to future results. Company fundamentals and earnings may be mentioned occasionally, but should not be construed as a recommendation to buy, sell, or hold the company’s stock. Predictions, forecasts, and estimates for any and all markets should not be construed as recommendations to buy, sell, or hold any security–including mutual funds, futures contracts, and exchange traded funds, or any similar instruments. The text, images, and other materials contained or displayed in this report are proprietary to Clearnomics, Inc. and constitute valuable intellectual property. All unauthorized reproduction or other use of material from Clearnomics, Inc. shall be deemed willful infringement(s) of this copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Clearnomics, Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Clearnomics, Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.